We’ve compared the best business savings account rates in the UK. You can compare rates on instant saver accounts, notice accounts and fixed term deposits from both established high street banks and newer online neobanks.

Featured: Tide

![]()

- Earn up to 4.00% AER (variable)** on your business savings

- Interest paid – 1st of every month (monthly)

- No min deposit amount, interest paid on up to £50,000 of business savings.

- Instant access to your money with no lock in period

- One of the leading providers of free business bank accounts

- Withdraw as often as you like

- All your savings are protected by the Financial Services Compensation Scheme (FSCS), covering up to a total value of £85,000.

- Track everything in app, in minute

Website: Click To Find Out More About Tide’s Business Savings Account

Featured: Revolut

![]()

- Earn between 2.15% and 3.30% AER depending on account type.

- Interest paid daily on both work and non-work days

- Add or withdraw money with zero restrictions 24/7

- Savings are deposited with trusted partner banks offering protection by the Financial Services Compensation Scheme (FSCS) up to £85,000

- Save up to £2m on their enterprise plan

- Interest only available on paid plans

- Offer accounts in 25+ different currencies

- Ability to accept card payments online and in-person

- Ability to control who has access to your account

Website: Click Here to learn about Revolut’s business savings products

Featured: Aldermore

- Earn 2.45% – 4.00% AER.

- Offers a choice of easy access or fixed-term accounts.

- Easy access accounts with flexible access.

- Fixed-terms of 6 months or 1 year.

- Minimum deposit of £1,000.

- Maximum balance of £1,000,000.

- Real-time interest rate information.

- Suitable for a variety of businesses including sole traders and small businesses.

- Rated ‘Excellent’ by Business Moneyfacts.

- Average independent review score of 4.7 out of 5.

Website: Aldermore Business Savings

Read the full Aldermore Business Savings Account review.

![]()

Companies are ranked in no particular order.

| Bank | Minimum Interest Rate (AER) | Maximum Interest Rate (AER) | Minimum term |

|---|---|---|---|

| Tide** | 3.35% | 4.00% | Instant Access |

| Revolut | 2.15% | 3.30% | Instant Access 24/7 |

| Aldermore | 2.45% | 4.00% | Instant access available |

| Virgin Money | 1.10% | 3.70% | Instant access available |

| HSBC | 1.21% | 1.41% | Instant access available |

| Wise | 1.75% | 3.41% | Instant access available |

| Barclays | 1.05% | 1.51% | Instant access available |

| NatWest | 0.85% | 2.75% | Instant access available |

| Lloyds | 0.50% | 2.66% | Instant access available |

| Metro Bank | 0.85% | 3.20% | Instant access available |

| Bank of Scotland | 0.50% | 2.66% | Instant access available |

| TSB | 1.35% | 2.80% | Instant access available |

| Santander | 0.40% | 2.20% | Instant access available |

| RBS (Royal Bank of Scotland) | 0.85% | 2.75% | Instant access available |

| Ulster Bank | 0.85% | 1.46% | Instant access available |

| Co-operative Bank | 1.06% | 3.43% | Instant access available |

| Allied Irish Bank | 0.25% | 2.26% | Demand Deposit |

| ICICI Bank UK | 1.60% | 3.60% | Instant access available |

| Nationwide | 0.00% | 3.73% | Instant access available |

| State Bank of India (UK) | 0.00% | 2.75% | Instant access available |

| United Trust Bank | 3.50% | 3.98% | Instant access available |

| Charity Bank | 2.94% | 3.61% | Instant access available |

| Kent Reliance | 3.81% | 3.81% | Instant access available |

| Cumberland Building Society | 2.20% | 3.65% | Instant access available |

| Redwood Bank | 3.80% | 3.95% | 35 days notice minimum |

| Shawbrook Bank | 3.40% | 3.92% | Instant access available |

| Cambridge Building Society | 1.55% | 3.50% | Instant access available |

| OakNorth | 2.35% | 3.50% | Instant access available |

| Carter Allen Private Bank | 2.20% | 3.85% | 35 days notice minimum |

| Saffron Building Society | 1.20% | 4.40% | Instant access available |

| Cambridge & Counties Bank | 4.05% | 5.00% | 31 days notice |

| Recognise Bank | 3.15% | 4.50% | Instant access available |

| Allica Bank | 2.80% | 4.00% | Instant access available |

| Monzo | 1.30% | 1.30% | Instant access |

* Note the interest rates above come from each company’s website and are subject to change at short notice. Therefore, you’ll need to visit them directly to the see their most up-to-date rates. Also be aware that the minimum interest rate is normally for their basic instant access accounts whereas the maximum rate will be for their fixed term accounts (sometimes up to 5 years).

- Earn 2.15%-3.30% AER.

- Interest paid daily on both work and non-work days

- Add or withdraw money with zero restrictions 24/7

- Earn up 4.00% AER (variable)

- Instant access to your money when needed

- No limits or fees on withdrawals

- Earn 2.45% – 4.00% AER.

- Offers a choice of easy access or fixed-term accounts.

- Average independent review score of 4.7 out of 5.

1. Virgin Money

![]()

- Earn 1.10%-3.70% AER.

- Offers a wide of business savings accounts.

- Choice of 2 easy access accounts that you can deposit and withdraw money when needed.

- Choice of notice accounts that you can top-up at anytime.

- Choice of fixed-rate for 3 months to 2 year account available.

- Notice periods of 30, 65, 95 and 120 days

- Limited online management.

- £1 minimum deposit.

- Maximum balance of £2,000,000 or £25,000,000 depending on the account.

- Can apply online if you have an business current account.

Website: Virgin Money Business Savings

Read the full Virgin Money Business Savings Account review.

2. HSBC

![]()

- Interest rates start at 1.21% AER

- Offers a choice of flexible accounts.

- Instant access with no access limits.

- No charges for transfers but cash and cheques transaction fees may apply.

- Call Accounts, Notice Accounts and Fixed Accounts are available.

- Minimum investment of £5,000 and no maximum investment.

- Option to benefit from UK money market interest rates.

- Client deposit account also available.

- Access your account via the internet, telephone and branches.

- Doesn’t require you to have a HSBC current account.

Website: HSBC Business Savings Accounts

Read the full HSBC Business Account review.

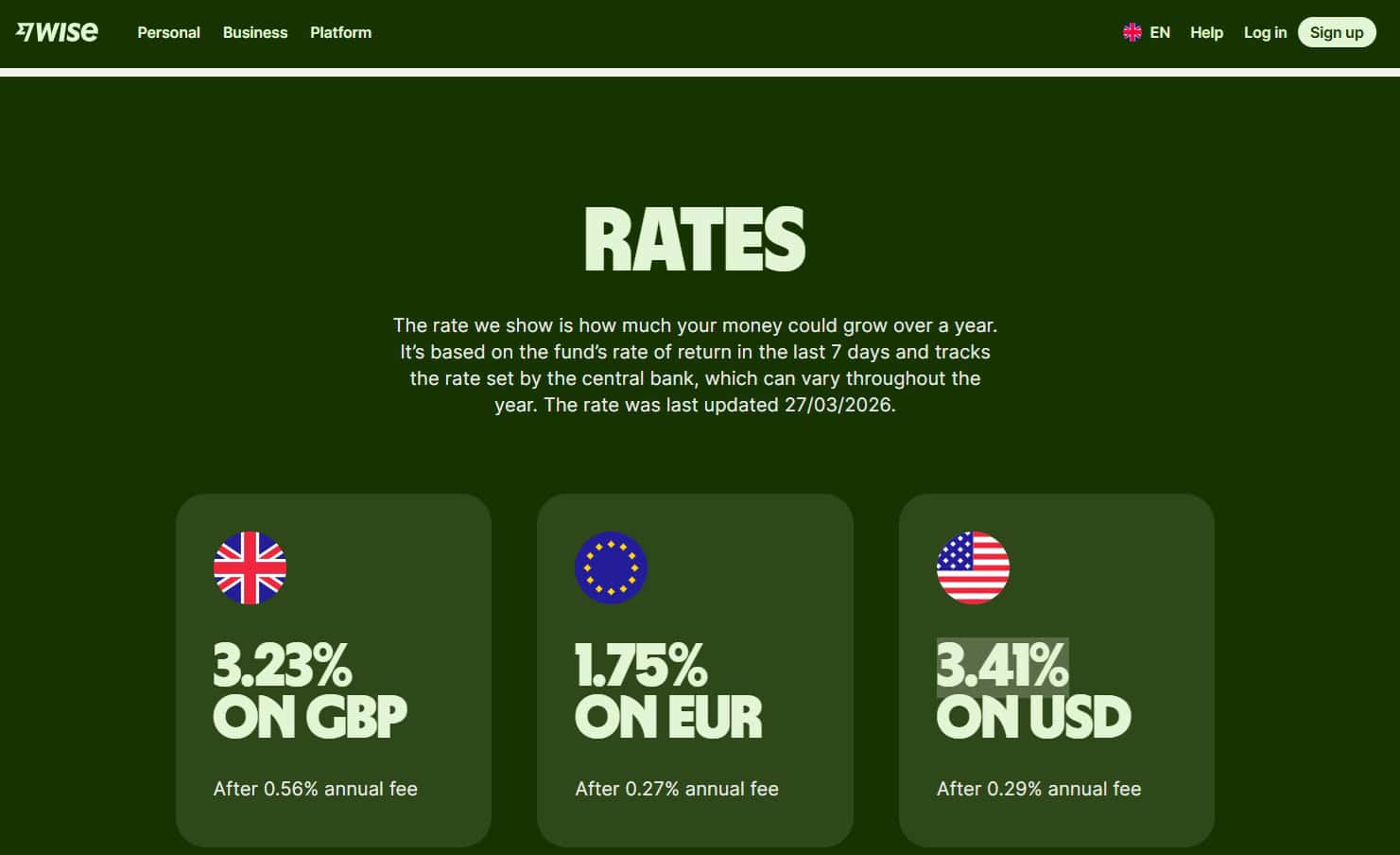

3. Wise

Note Wise is not a bank and it holds its savings funds via Blackrock. You can learn more here.

- Currently offering 3.23% on GBP for Instant access accounts.

- Offering 3.41% on USD deposits

- Offering 1.75% on EUR deposits

- No hidden fees of monthly subscriptions

- Costs £45 to open an account

- 0.5% Cashback available to some customers

- Can hold up to 50 currencies (interest only paid on GBP, USD & EUR)

- Used by 300,000+ businesses each quarter

- Authorised by the FCA

- Connects to Xero, QuickBooks, & FreeAgent

- Rated 4.4 out of 5 on Trustpilot

Website: Wise Business Website

Read full Wise review

5. Barclays

![]()

- Earn up to 1.51% AER on instant access and client deposit.

- Offers a range of business savings accounts.

- Instant access account with no minimum balance.

- Client deposit account allows instant access to funds.

- Fixed-term accounts with no access for an agreed term.

- £100,000 minimum balance and maximum of £24,999,999 on fixed-term accounts.

- Interest rates on fixed-term accounts depend on term and will be discussed on application.

- Manage instant access and client deposit online, branch and over the phone.

- Manage fixed-term account in branch or over the phone.

- Apply online, in branch or over the phone.

Website: Barclays Business Savings Accounts

Read the full Barclays Business Account review.

6. NatWest

![]()

- Earn 0.85%-2.75% AER on the easy access and notice accounts.

- Offers a wide choice of business savings accounts.

- Instant access with no minimum or maximum balance.

- Notice account with 35 days notice for access with no minimum or maximum balance.

- Fixed-term savings for tailored terms up to 12 months.

- Client accounts are also available.

- Fixed-term account minimum balance starts at £100,000 with no maximum.

- Fixed-term account interest rate is agreed when you open the account and paid at the end of term.

- Interest is applied daily on many of the accounts.

- You can apply online.

Website: NatWest Business Savings Accounts

Read the full NatWest Business Account review.

7. Lloyds Bank

![]()

- Instant access interest rates from 1.21% AER.

- Fixed Term Deposit up to 2.66% AER

- Offers a choice of instant access and fixed-term savings accounts.

- Instant access with a minimum balance of £1.

- Choice of fixed-term from overnight to 3 years.

- Notice accounts with either 32 or 95 days notice periods.

- Deposit £1 to £5,000,000.

- Unlimited withdrawals on instant access and notice accounts.

- View and manage your account online.

- Provides a savings strategy tool to help you to manage your savings.

- You can apply online if you have an account with them.

Website: Lloyds Bank Business Savings Accounts

Read the full Lloyds Bank Business Account review.

8. Metro Bank

![]()

- Earn from 0.85%-3.20% AER.

- Offers business and community deposit accounts.

- Instant access deposit accounts for businesses or community groups and charities.

- Fixed-term deposit accounts for 1 or 2 years from £5,000.

- Notice accounts with a choice of fixed periods.

- Periods of 35, 60 or 95 days’ notice available.

- No setup fees.

- Some charges for dealing with cheques.

- Client deposit accounts are also available.

- Business owners can open an account in-store.

Website: Metro Bank Business Savings Accounts

Read the full Metro Bank Business Account review.

9. Bank of Scotland

![]()

- Interest rates 0.50%- 2.66% AER.

- Offers a choice of instant access and fixed-term savings.

- Instant access with flexible access with a minimum balance of £1.

- Notice accounts offering unlimited withdrawals.

- Fixed-term accounts are available.

- Save from £10,000 -£5,000,000

- Choice of 32 or 95 days notices on notice accounts.

- Choose your own fixed term for up to 2 years.

- Manage your accounts online.

- Existing customers can apply online.

Website: Bank of Scotland Business Savings Accounts

Read the full Bank of Scotland Business Account review.

10. TSB

![]()

- Earn from 1.35% to 2.80% AER, depending on your balance.

- Offers an instant access savings account only.

- Requires a balance of £5,000 or more to earn higher interest rates.

- Interest is calculated daily and applied monthly.

- Minimum opening balance of £1.

- Can withdraw instantly but daily limits apply.

- Manage the account online 24/7.

- Can also manage the account in branch and over the phone.

- Open and manage your account online or in-branch.

- You don’t have to be an existing customer.

Website: TSB Business Savings Accounts

Read the full TSB Business Account review.

11. Santander

![]()

- Earn from 0.40%-2.20% AER.

- Offers instant access and longer term savings accounts.

- Instant access savings for a simple easy access account.

- Business Reward Saver offers higher interest for not making withdraws but is still easy access.

- Fixed-rate bond accounts with a 1 year term.

- Also offers treasurer’s account.

- Minimum deposit of £1 on instant access and Business Reward Saver and £5,000 on fixed-rate.

- Maximum savings of £5,000,000.

- Manage your account online, over the phone, and in-branch.

- Preferential rates for customers who already have a 1|2|3 Business World current account.

Website: Santander Business Savings Accounts

Read the full Santander Business Account review.

12. RBS (Royal Bank of Scotland)

![]()

- Earn from 0.85% – 2.75% AER.

- Offers a choice of instant access and longer term savings accounts.

- Instant access with no withdraw or balance restrictions.

- Notice account to lock away funds for 35 days.

- Fixed-term accounts with a choice of term.

- Terms of overnight to 12 months with rates reflecting the length.

- Interest rates for fixed-term accounts vary based on the term and available on application.

- Minimum balance of £100,000 on fixed-term account.

- No minimum balance for the instant access and notice accounts.

- No maximum balance on any of the accounts.

Website: Royal Bank of Scotland Business Savings Accounts

Read the full Royal Bank of Scotland Business Account review.

13. Ulster Bank

![]()

- Earn from 0.85% to 1.46% AER

- Offers a variety of business savings products.

- Instant access savings providing flexibility.

- Fixed-term accounts with a choice of term lengths.

- Foreign currency savings account also available.

- Terms from 1 week to 1 year.

- Most rates are not published but available on request.

- Interest is calculated daily and applied monthly on the instant access account.

- No withdrawal limits or balance restrictions on the instant access account.

- No maximum balance limits.

Website: Ulster Bank Business Savings Accounts

Read the full Ulster Bank Business Account review.

14. Co-operative Bank

![]()

- Earn 1.06%-3.43% AER.

- Offers a choice of instant access and notice accounts.

- Notice accounts offering either 35 or 95 days notice period.

- Instant access for straightforward savings.

- Allows a lump sum or regular deposits.

- Manage your instant access account online and over the phone.

- Manage the notice account over the phone only.

- No minimum or maximum balance needed.

- Download an application and post it to them or return to a branch.

- Must be a Co-operative business current account customer.

Website: Co-operative Bank Business Savings Accounts

Read the full Co-operative Bank Business Account review.

15. Allied Irish Bank

![]()

- Earn from 0.25% to 2.26% AER

- Offers fixed-term and demand deposit accounts.

- Fixed-term deposit with a minimum £5,000 deposit.

- Terms from 1 week to 5 years.

- Demand deposit accounts providing instant access.

- Interest is calculated daily and credited monthly or quarterly on demand deposit accounts.

- Interest on fixed-rate accounts is calculated daily but applied annually or at the end of the term.

- Interest rates on fixed-term accounts is agreed when you open the account.

- Existing customers can open an account with their Relationship Manager.

- New customers can open an account in branch.

Website: Allied Irish Bank Business Savings Accounts

Read the full Allied Irish Bank Business Account review.

16. ICICI Bank UK

- Earn 1.60% AER (variable) on business savings accounts

- Earn up to 3.60% AER on fixed term deposits

- Offers easy access and fixed deposit savings accounts.

- Easy access

- Fixed deposit accounts that are available in dollars or sterling.

- Terms of 6 months, 1, 2, 3 or 5 years.

- Save with just £1.

- Maximum savings of £5,000,000 (easy access) or £1,000,000/$1,000,000 (fixed deposit).

- Manage your account online (easy access only) and in branch.

- Must hold a business current account with them.

- Apply in branch only.

Website: ICICI Bank UK Business Savings

Read the full ICICI Bank UK Business Savings Account review.

17. Nationwide

![]()

- Earn 1.50% AER on instant access accounts (must keep at least £5,000 in your account at all times)

- Earn 3.73% AER on 6 month Saver.

- Earn interest either monthly or annually

- Easy access account with withdrawals and deposits at any time although minimum withdrawal is £500.

- Only currently offering Instant Access accounts

- £5,000 minimum opening balance.

- Save up to £10 million

- Manage your account by email, post or fax

- No fees or charges

- The interest rate is variable

Website: Nationwide Business Savings

Read the full Nationwide Business Savings Account review.

18. State Bank of India (UK)

![]()

- Earn up to 2.75% AER.

- Offers Instant Access, Limited Access, 35 Day Notice, and Fixed Term Deposit Accounts

- Requires a minimum balance of £10,000.

- Interest will not be paid if balance falls below £10,000.

- Allowance of 25 free transactions per month.

- Available in pounds (GBP) and US dollars (USD).

- Interest is paid at the end of each month.

- Only offered to micro-enterprises with fewer than 10 employees.

- Manage everything in-branch, online, and in the post.

- Annual fee applies, unless your balance is £10,000 or more.

Website: State Bank of India UK Business Savings

Read the full State Bank of India UK Business Bank Account review.

19. United Trust Bank

- Earn 3.50%-3.98% AER.

- Offers easy access, fixed-rate and notice accounts.

- Terms of instant up to 3 years.

- Withdrawals during the term are not allowed.

- Minimum deposit of £5,000.

- Maximum deposit is £1,000,000.

- Interest is accrued and paid annually.

- 14-days notice will be give before the end of the term.

- At the end of the term you can re-invest or nominate an account for a transfer.

- You can open an account online or through the post.

Website: United Trust Bank Business Savings

Read the full United Trust Bank Business Savings Account review.

20. Charity Bank

- Earn from 2.94% to 3.61% AER

- For their easy access account if your balance falls below £10,000 they’ll pay you just 0.10% AER

- Allows you to support UK-based charities and community enterprises while you save.

- Offers easy access, notice accounts and fixed rate accounts

- No withdrawals during the term.

- Also offers accounts for charities, clubs and credit unions

- £1,000 minimum deposit.

- Maximum deposit of £500,000.

- Manage your account by post, email, and phone.

- At the end of term you can re-invest the funds or nominate an account to transfer it to.

Website: Charity Bank Business Savings

Read the full Charity Bank Business Savings Account review.

21. Kent Reliance

![]()

- Earn 0.10% – 5.16% AER.

- Offers easy access savings account and notice accounts.

- £1,000 minimum deposit but minimum operating balance is £1.

- Maximum deposit £1,000,000.

- Interest is paid either monthly or annually.

- Can only open an account online if you have an exiting account with them

- Manage your account easily online.

- Access your savings whenever needed.

- Branches only in the South East of England.

- You must have a maximum of 3 directors.

Website: Kent Reliance Business Savings

Read the full Kent Reliance Business Savings Account review.

22. Cumberland Building Society

- Earn 2.205% – 3.65% AER.

- Offers a range of business savings accounts.

- Instant Access account with a minimum £100 balance.

- eSavings account that is an instant access account with a £1 minimum balance.

- Notice account with a minimum balance of £10,000.

- Maximum account balance of £1,000,000.

- Give 40 days’ notice on the notice account.

- Secure a higher interest rate if you’re an internet banking customer.

- Accounts can be opened in branch, online or over the phone.

- You must live in their operating area to be eligible.

Website: Cumberland Building Society Business Banking

Read the full Cumberland Building Society Business Bank Account review.

23. Redwood Bank

- Earn 3.80% – 3.95% AER.

- Offers longer term savings options.

- Choice of notice accounts.

- Fixed-rate account for 1-year.

- Access your funds with 35 or 95 days’ notice on notice accounts.

- Interest can be paid monthly or annually.

- £10,000 minimum deposit.

- Maximum deposit of £1,000,000.

- Awarded Best Business Fixed Rate Bond Provider 2019 and 2020.

- Apply for an account online in 15 minutes.

Website: Redwood Bank Business Savings

Read the full Redwood Bank Business Savings Account review.

24. Shawbrook Bank

![]()

- Earn 3.40% – 3.92% AER.

- Offers a range of business savings accounts.

- Easy access accounts with flexible saving facilities.

- Notice accounts with 45 and 100 days notice.

- Fixed-rate accounts for 1 or 2 years.

- £1,000 minimum balance.

- Maximum balance of £2,000,000.

- Lock away your funds for higher rates.

- Suitable for sole traders, partnerships and limited companies.

- Not available to charities or trusts.

Website: Shawbrook Bank Business Savings

Read the full Shawbrook Bank Business Savings Account review.

25. Cambridge Building Society

- Earn from 1.55% to 3.50% AER

- Offers easy access accounts, Notice Accounts and 1 year fixed term savings bonds

- Withdraw from easy access account up to twice a month.

- £1,000 minimum investment.

- Maximum balance of £2,500,000.

- Manage your account in branch or by post.

- View your account in their app.

- Interest is calculated daily and paid annually at the end of the year.

- Open an account in branch, over the phone or through the post.

- Available to sole traders, partnerships, limited companies, charities, clubs and housing associations.

Website: Cambridge Building Society Business Savings

Read the full Cambridge Building Society Business Savings Account review.

26. OakNorth

- Earn 3.50% AER.

- Offers only one business savings account type

- Easy access account with next day access.

- Interest rates are variable and can be increased or decreased.

- Can only access your Earn Vault via the mobile app

- Currently has a waiting list

- No minimum or maximum deposit limits apply

- You can only add money to your Earn Vault from your current account.

- Manage your account online.

- Average Feefo rating of 4.5/5.

Website: OakNorth Business Savings

Read the full OakNorth Business Savings Account review.

27. Cater Allen Private Bank

![]()

- Earn 2.20% to 3.85% AER.

- Offers a Fixed Term Deposit Account and;

- Notice account with 35 days notice.

- Unlimited withdrawals allowed.

- £0 minimum deposit.

- Highest interest rates paid on balances over £5m

- Withdrawals without any charges. Just provide 35 days’ notice

- Manage your account online, over the phone, and through the post.

- Suitable for sole traders, partnerships, limited companies, charities, clubs and societies.

- Part of the Santander Group.

Website: Cater Allen Private Bank Business Savings

Read the full Cater Allen Business Savings Account review.

28. Saffron Building Society

![]()

- Interest rates from 1.20% to 4.40% AER.

- Offers a choice of instant access and longer-term savings options.

- eSaver account with easy access and a minimum deposit of £10,000.

- An instant saving account with a minimum opening deposit of £1.

- 1-year fixed savings account with a minimum deposit of £5,000.

- Sports and social clubs account with an opening deposit of £1.

- Minimum deposit levels vary per account.

- Interest is paid annually on most accounts.

- Branches in the South East of England only.

- Some accounts managed online, others in-branch and through the post.

Website: Saffron Building Society Business Savings

Read the full Saffron Building Society Business Savings Account review.

29. Cambridge & Counties Bank

![]()

- Earn 4.05%-5.00% fixed AER

- Offers a choice of longer-term business savings account.

- Choice of fixed-rate business, trust and charity bond accounts.

- Terms of 31 days, 95 days or 1, 2, 3 or 5 years on fixed-rate accounts.

- Minimum investment of £10,000.

- Maximum investment of 5,000,000 or £3,000,000 on notice account.

- No withdrawals are allowed until the account matures or the notice period is up.

- Open to sole traders, limited companies, charities, and clubs.

- ‘Best Business Fixed Rate Bond Provider’ at the Savings Champion Awards 2020.

Website: Cambridge & Counties Bank Business Savings

Read the full Cambridge & Counties Bank Business Savings Account review.

30. Recognise Bank

![]()

- Earn 3.15%-4.50% AER

- Offers a range of business savings accounts

- Easy access account

- 95-day notice account

- 1 year fixed rate account

- Minimum deposit of £1,000

- Maximum savings across all your accounts of £85,000

- Online account management

- Up to four named people can access the account

- Available to small to medium-sized businesses with less than 250 employees

Website: Recognise Bank Business Savings

31. Allica Bank

- Earn up to 4.00% AER on a 12-month fixed term savings account.

- Easy access account offers 2.80% AER

- Rate is guaranteed

- Can apply online

- FSCS protected up to £85k

- Can invest between £10,000 and £2,000,000

- Do not accept CHAPS payments

- Will get in contact 30 days before maturity to discuss next steps

- No fees to use the account

- Must be a UK based business

Website: Allica Bank Business Savings

32. Monzo

![]()

- Earn 1.30% AER interest (variable) on your spare money

- Protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per person

- Schedule regular payments in to your savings pot for future needs

- Interest paid monthly

- No minimum deposit

- Must meet their eligibility criteria

- Must be an existing Monzo Business customer

- Sign up from your phone tor online

Website: Monzo Business Savings

FAQ

Who can get a business savings account in the UK?

In the UK, business savings accounts are available to a wide range of businesses, including but not limited to:

Sole Traders: Individuals running their own business alone. They can open a business savings account to manage their business finances separately from their personal finances.

Partnerships: Businesses operated by two or more individuals. Both general partnerships, where all partners share liability, and limited partnerships, where some partners have limited liability, can apply for business savings accounts.

Limited Companies (Ltd): Companies where the liability of the shareholders is limited to their investment. Both small and medium-sized enterprises (SMEs) and larger companies can benefit from business savings accounts.

Limited Liability Partnerships (LLP): A partnership in which some or all partners (depending on the jurisdiction) have limited liabilities. It exhibits elements of both partnerships and corporations.

Charities and Not-for-Profit Organizations: Charitable organizations can also open business savings accounts to manage donations and funding more effectively.

Clubs, Societies, and Associations: Informal groups or formal clubs with financial activities or savings can open a business savings account to better manage their funds.

The eligibility criteria can vary between banks and financial institutions. Generally, to open a business savings account, an organization will need to provide:

Proof of business registration and operation in the UK (e.g., company registration number for limited companies, partnership agreement for partnerships).

Identification and address verification for the key individuals in the business, such as owners, partners, or directors.

Details about the nature and financial situation of the business.

Some banks may have specific requirements based on the business’s turnover, the amount to be deposited, or the length of time the business has been in operation.

It’s also common for banks to conduct a credit check on the business or its principals. It’s advisable to check with the specific bank or financial institution for their particular requirements and to compare the features, benefits, and restrictions of their business savings accounts to find the best fit for your business’s needs.

Why open a business savings account?

Having savings can help your business prepare for future investments, secure the future, and make it easier to afford essentials.

Opening a dedicated savings account is a good idea because you can earn interest on your balance, meaning your business’ cash earns while it sits there doing nothing.

How do business savings accounts work?

The more you save and the longer the period, the more interest you’ll earn on your balance. Savings accounts are usually instant access, notice, or fixed term.

Instant access accounts are exactly what they sound like – you can withdraw and pay in at any time.

Notice accounts require you to give a period of notice before you withdraw, typically between 30 and 120 days.

Fixed-term accounts (sometimes also called Business Bonds) usually offer higher interest rates than easy access accounts, but you can’t withdraw any of the cash until the fixed period ends, these can be fixed for short periods through to 5 years but the longer the length the higher the interest rate normally is.

What are the differences between a business savings account and a business bank account?

A savings account is designed specifically for depositing money for later, whether you’ll need it in a couple of weeks or a couple of years. A business current account is for everyday business spending and earning.

Current accounts don’t usually earn interest on the balance. If they do, the rate will often be a lot lower than the rate you’d get with a savings account.

How to open a business savings account?

You can often apply for a business savings account online, but depending on the account and the provider, you might be restricted to applying over the phone or in person.

You’ll often need to deposit an amount to open your account, which can range from just £1 to several thousand pounds.

What interest rates do business savings accounts currently offer?

With the Bank of England continuing to raise interest rates, rates for savings accounts have also been increasing.

Business savings accounts in the UK currently offer interest rates of between 0.10% AER all the way up to 5.00% AER. These rates depend on whether you want an instant access account, a notice account or a fixed term account.

You’ll usually get a higher interest rate if you save for a fixed period, compared to instant access.

How long do you have to keep money in a business savings account?

How long you save for is entirely up to you. To earn the best return, it makes sense to save for at least a year.

If you want to keep your money accessible, an instant access or notice account is the best option. This means you can save your money for as long as you want.

Who offers the best business savings account?

The best business savings account for your business depends entirely on how much you want to save and when and how you want to access your money.

– Wise currently offers the highest interest rate on a business instant access account at 4.66% AER. However, they are not a bank and the money itself is invested via a Blackrock fund.

– In terms of banks, Tide has the highest instant access rate at 4.33% AER and the money is fully protected by the Financial Services Compensation Scheme (FSCS), up to a total value of £85,000.

United Trust’s Business 180d Notice Base Rate Tracker offers a 5.25% AER variable rate which is the highest rate from any of the banks and financial institutions listed above.

Here are the highest rates for other popular types of accounts:

– 95 Day Fixed Rate: United Trust Bank at 4.99% AER

– 180 Day Notice Tracker Account: United Trust Bank at 5.25% AER

– 1 Year Fixed Rate: Virgin Money at 5.05% AER

– 2 Year Fixed Rate: United Trust Bank at 4.85% AER

– 5 Year Fixed Rate: Cambridge & Counties Bank & United Trust at 4.30% AER

What is the current Bank of England base rate?

The latest Bank of England base rate is: 5.25%, this is up from a low of 0.1% in 2021.

What is the difference between a business savings account and Gilts?

A business savings account and gilts (government bonds) are two different financial instruments that serve different purposes for investors or savers.

Here are the key differences:

Nature and Purpose:

Business Savings Account: It’s a type of savings account aimed specifically at businesses, allowing them to earn interest on their surplus cash while still having access to their funds. These accounts are offered by banks and other financial institutions.

Gilts: These are government bonds issued by the UK Government. When you buy gilts, you are effectively lending money to the government. In return, the government promises to pay you a fixed rate of interest (coupon) and to return the principal on a specified date (maturity).

Risk:

Business Savings Account: Generally considered low risk because they are savings accounts, and are protected by up to £85,000 by FSCS deposit insurance. The principal amount is safe, and the interest rate is usually fixed or variable.

Gilts: Also considered low risk, especially when compared to corporate bonds or stocks, because they are backed by the government. However, their value can fluctuate based on interest rate movements and inflation expectations. If sold before maturity, they may yield less than the purchase price if interest rates have risen.

Return:

Business Savings Account: Offers a return in the form of interest on the deposited funds. The interest rates are often lower than those you might expect from investments in the stock market or bonds but offer safety and liquidity.

Gilts: Provide a return through regular interest payments until maturity, and the principal is returned at maturity. The interest rate (yield) on gilts can vary depending on the term of the bond and market conditions.

Liquidity:

Business Savings Account: High liquidity, allowing businesses to withdraw funds as needed, though there may be some restrictions or fees depending on the account’s terms.

Gilts: They can be sold in the secondary market before maturity, providing some liquidity. However, the price you receive depends on the current market conditions and may result in a capital gain or loss.

Usage:

Business Savings Account: Used by businesses to manage cash flow and save excess cash with some interest earnings. It’s a tool for cash management and short-term savings.

Gilts: Often used by investors seeking a low-risk investment or looking to diversify their investment portfolio. They are suitable for long-term savings, especially for those seeking fixed income.

Both business savings accounts and gilts offer low-risk opportunities to park funds, but they cater to different needs and offer different benefits and drawbacks related to risk, return, liquidity, and purpose.

* Note we have affiliate relationships with Tide, Aldermore, Virgin Money, HSBC, Starling and Wise.