What Is A VAT Threshold?

A VAT threshold or VAT registration threshold, refers to the level of annual sales turnover at which businesses are required to register for VAT (value-added tax). When a business reaches or exceeds the VAT-taxable turnover, it becomes a legal requirement for them to register for VAT.

How Much Is The VAT Threshold In The UK?

The current VAT registration threshold for the UK is £85,000. This threshold has been in place since 2017 and is expected to remain unchanged until 2024.

Once a business’s turnover reaches the VAT registration threshold, they have 30 days to register for VAT with HMRC. After the business is VAT registered, it will have new responsibilities. These responsibilities include:

- Charging VAT on their products and services

- Paying VAT on goods and services received from vendors

- Submitting VAT returns to HMRC annually

- Maintaining VAT accounts and records

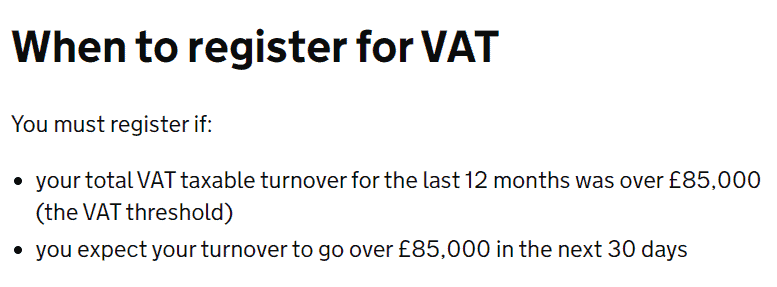

When To Register For VAT

According to the HMRC guide on when to register for VAT, there are several instances in which you will be required to register. Instances where VAT registration is required include:

- If your total VAT taxable turnover reaches more than £85,000 in a 30-day period

- If your total turnover was £85,000 at the end of any given month in the last year

- If you take over a VAT-registered business

In some cases, you will need to be VAT-registered regardless of your turnover. This is true if the following criteria are met:

- You supply goods and services to the UK or you’re planning to do so in the next 30 days

- You’re based outside of the UK

- Your business is based outside of the UK

If your goods and services are exempt from VAT, you do not have to register or pay VAT. However, it’s best to ensure that you know what goods are exempt from VAT and which aren’t.

It’s also important to remember that you can opt for ‘voluntary VAT registration’ if your turnover is under £85,000. This means that you will register for VAT while having no legal obligation to do so.

VAT Accounting Schemes

VAT accounting schemes offer businesses different ways to better control their VAT obligations. These schemes come with specific VAT thresholds that determine eligibility for each scheme.

While the VAT registration threshold mandates registration once taxable turnover reaches a certain amount, participation in accounting schemes is optional.

VAT Flat Rate Scheme

The VAT Flat Rate Scheme is one where businesses pay a fixed rate of VAT to HMRC. To join this scheme, a company must have a taxable turnover of less than £150,000.

If a business becomes part of the Flat Rate Scheme, it must leave the scheme if its turnover exceeds the compulsory VAT deregistration threshold of £230,000.

VAT Cash Accounting Scheme

The VAT Cash Accounting Scheme follows the same principles as cash accounting. With this, businesses record and pay their VAT when money changes hands rather than when invoices are issued or received.

To join this scheme, a business must have a VAT-taxable turnover of £1.35 million or less. There is also a mandatory VAT deregistration threshold, and businesses must leave the scheme if their turnover exceeds £1.6 million.

Annual Accounting VAT Scheme

The Annual Accounting Scheme allows businesses to submit one VAT return per year and make advance payments toward their VAT bill. Eligibility for this scheme requires a turnover of £1.35 million or less.

Much like with the Cash Accounting Scheme, businesses must deregister if their turnover exceeds £1.6 million.

FAQs

What are the benefits of accounting schemes for VAT?

These schemes can simplify record-keeping, provide cash flow advantages, and reduce administration for businesses.

Can I change between accounting schemes for VAT?

Yes, you can change between accounting schemes for VAT. However, this is provided you meet the eligibility criteria for the scheme you want to switch to.

Final Thoughts

Understanding VAT thresholds and registration is crucial for businesses to ensure compliance with tax regulations, which is why it is useful to employ the help of a professional accountant. While the VAT registration threshold determines when a company must register for VAT, accounting schemes offer other ways to manage your VAT.

By knowing the thresholds and available schemes, you can make more informed decisions and effectively handle your VAT obligations.

References

https://www.sumup.com/en-gb/invoices/dictionary/vat-threshold/

https://startups.co.uk/tax/when-do-you-need-to-register-for-vat/